Nawal A. Khaleel1, Salem H. Almadhun2 , Hanan A. Khalil3, Abdalla M. Alasoud4, Aimen M. Rmis5

1 Department of Information Technology, Faculty of Science and Nature Resources, Al Jafara University; nawalnasar90@gmail.com

2 Department of Computer, Faculty of Education, Elmergib University, Al Khums, Libya; salem.almadhun@elmergib.edu.ly

3 Department of Information Technology, Faculty of Science and Nature Resources, Al Jafara University; khlilhanan811@yahoo.com

4 Department of Computer Science, Faculty of Science, Alasmarya Islamic University, Zliten, Libya; ab.alasoud@asmarya.edu.ly

5 Department of Computer Science, Faculty of Science, Alasmarya Islamic University, Zliten, Libya;

HNSJ, 2023, 4(8); https://doi.org/10.53796/hnsj4818

Published at 01/08/2023 Accepted at 20/07/2023

Abstract

Mobile banking services have witnessed a significant growth in recent years and become a popular way of conducting financial transactions. Libya, like many other countries, has also experienced a similar trend, where mobile banking services are becoming more prevalent. This abstract will discuss the current state of mobile banking services in Libya. The study focuses on the adoption and usage of mobile banking services in Libya. The research methodology employed a mixed-method approach, including a survey questionnaire and interviews with industry experts. The sample consisted of 420 mobile phone users in Libya who have used mobile banking services before. The study’s data was analyzed using the software package for social science SPSS V.25. The study’s findings abundantly supported the notion that perceived utility and consideration of ease of use, trust, social norms, and perceived risk had a direct and beneficial impact on the uptake of mobile banking. The study also identified several factors that could drive the adoption of mobile banking services in Libya, including increasing awareness campaigns about the service, improving the security and reliability of the service, and offering incentives to encourage more users to adopt the service. The study recommends that the bank should consider age differences and educational levels of customers while providing adequate and detailed explanations for older age groups and customers with lower educational levels. This will make them more acceptable and desirable to adopt mobile banking services.

Key Words: Mobile banking, customer satisfaction, intention to use, perceived risk, social norms, perceived trust.

Mobile banking technology has revolutionized the way customers interact with their banks and manage their finances. With the widespread adoption of smartphones and tablets, mobile banking has become an increasingly popular way for customers to access their accounts, transfer funds, pay bills, and more. According to a report by Research and Markets, the global mobile banking market is expected to grow at a CAGR of 22.2% from 2021 to 2026, driven by factors such as the increasing adoption of smartphones, rising internet penetration, and the need for convenient and secure banking services (Kshetri, N. 2018 ).

The emergence of mobile banking technology has provided several benefits for both banks and customers. For banks, mobile banking has enabled them to reduce costs by shifting transactions from traditional branches to digital channels. It has also allowed banks to improve customer engagement by providing a more convenient and personalized banking experience. For customers, mobile banking has provided a more convenient and accessible way to manage their finances, allowing them to perform transactions anytime, anywhere.

However, the adoption of mobile banking technology also presents several challenges. One of the major challenges is ensuring the security and privacy of customer data. With the rising number of cyber threats and data breaches, ensuring the safety of customer information has become a top priority for banks and financial institutions. Another challenge is overcoming the resistance to change from customers who prefer traditional banking methods( Osamah Alhadi A. Alloush, Mahendrawathi, ER. 2020). Despite these challenges, the adoption of mobile banking technology is expected to continue to grow in the coming years. As more customers become comfortable with digital channels and demand more convenient and personalized banking services, banks and financial institutions will need to continue to innovate and invest in mobile banking technology to remain competitive. Mobile banking technology enables customers to perform banking transactions using their mobile devices, such as smartphones and tablets. These transactions can include checking account balances, transferring funds, paying bills, and even applying for loans or opening new accounts. Mobile banking technology has become increasingly popular in recent years, as more and more customers have adopted smartphones and tablets as their primary means of accessing the internet (Research and Markets 2021).

One of the key benefits of mobile banking technology is its convenience. Customers can perform banking transactions anytime, anywhere, without the need to visit a physical bank branch. This has made banking more accessible for customers who may not have easy access to traditional banking services.

Paper hypotheses:

This paper proposes the following hypotheses:

- H1: The perceived usefulness of mobile banking has a significant positive impact on users’ intention to use it.

- H2: The perceived ease of use of mobile banking has a significant positive impact on users’ intention to use it.

- H3: The perceived trust in mobile banking has a significant positive impact on users’ intention to use it.

- H4: Social norms have a significant positive impact on users’ intention to use mobile banking.

- H5: The perceived risk associated with using mobile banking has a significant negative impact on users’ intention to use it.

- H6: The degree to which consumers are satisfied with the service is significantly influenced by their propensity to use mobile banking.

Paper questions:

The current research study aims to investigate the following main question:

What factors influence users’ intention to use mobile banking services and how do they affect customer satisfaction?

To answer the main question, the following sub-questions are proposed:

- How does the perceived usefulness of mobile banking affect users’ intention to use it?

- How does the perceived ease of use of mobile banking affect users’ intention to use it?

- How does perceived trust in mobile banking affect users’ intention to use it?

- How do social norms influence users’ intention to use mobile banking?

- How does perceived risk associated with using mobile banking affect users’ intention to use it?

- How does users’ intention to use mobile banking affect their satisfaction with the service?

- literature review and previous study:

Mobile banking has emerged as a popular way for customers to access their bank accounts and perform financial transactions. With the increasing adoption of smartphones and tablets, mobile banking has become more accessible and convenient for customers. This literature review aims to provide an overview of the existing literature on mobile banking, including its benefits, challenges, and previous studies. Several studies have identified the benefits of mobile banking, including its convenience, accessibility, and personalized banking experience. For example, a study by KPMG found that 70% of customers who used mobile banking felt that it saved them time and enhanced their banking experience. Another study by McKinsey & Company found that mobile banking could reduce transaction costs for banks by up to 90%.

Despite the benefits of mobile banking, several challenges also exist. One of the major challenges is ensuring the security and privacy of customer data. With the increasing number of cyber threats and data breaches, banks must take steps to ensure that customer data is protected. Another challenge is overcoming the resistance to change from customers who prefer traditional banking methods ( Hanan A. Khalil, 2023 & Topcu, 2020). Several studies have investigated the factors influencing the adoption of mobile banking. For example, a study by Liao and Cheung found that perceived usefulness and ease of use were significant factors influencing the adoption of mobile banking in Hong Kong. Another study that trusts and perceived risk were significant factors in the adoption of mobile banking in Taiwan. A recent study by Shang and Deng found that the perceived usefulness and ease of use of mobile banking were significant factors influencing the adoption of mobile banking in China (Shang, S. S., & Deng, Z. 2014 & Rmis et al., 2020).

This study (Al-Sukkar, A., & Al-Wesha, S. (2019), aims to identify the factors influencing the adoption of mobile banking in Jordan. The authors conducted a survey of 500 Jordanian bank customers to collect data on their adoption of mobile banking and their attitudes towards it. The study identified several factors that influence the adoption of mobile banking, consisting of perceived utility, perceived ease of use, perceived danger, trust, and social impact. The study found that perceived usefulness and perceived ease of use were the most significant factors influencing the adoption of mobile banking. Other important factors included trust in the bank and social influence. Perceived danger, according to the report, is a key deterrent to the use of mobile banking.

In summary, the study offers insightful information on the variables impacting Jordan’s adoption of mobile banking. Banks and financial institutions can use this information to develop effective marketing strategies and improve their mobile banking services to increase their customer base. This study (Adomako, S., Danso, A., & Damoah, I. S. (2018), aims to identify the determinants of mobile banking adoption in Ghana. The authors conducted a survey of 400 bank customers in Ghana to collect data on their adoption of mobile banking and their attitudes towards it. The study identified several determinants of mobile banking adoption, including confidence social influence, perceived utility, perceived usability, and demographic characteristics. The investigation indicated that the most important factors influencing the adoption of mobile banking were perceived utility and perceived simplicity of use. Other important determinants included trust in the bank, social influence, and demographic factors such as age, income, and education level. The study also found that security concerns were a significant barrier to the adoption of mobile banking.

As a whole, the investigation offers useful details about Ghana’s use of mobile banking. Banks and financial institutions can use this information to develop effective marketing strategies and improve their mobile banking services to increase their customer base in Ghana. The Authors: (Singh, P., & Srivastava, R. K. 2018), identify the factors influencing the adoption of mobile banking in India. The authors conducted a survey of 400 bank customers in India to collect data on their adoption of mobile banking and their attitudes towards it. The study identified several factors that influence the adoption of mobile banking, including perceived usefulness, perceived ease of use, trust, social influence, and demographic factors. According to the survey, perceived utility and perceived simplicity of use are the main variables influencing the uptake of mobile banking. Other crucial elements were social influence, bank trust, and demographics including age, income, and educational attainment. A big hurdle to the use of mobile banking, in accordance with the survey, was security worries. In broadly, the report offers helpful knowledge into the variables impacting India’s adoption of mobile banking technologies. Banks and financial institutions can use this information to develop effective marketing strategies and improve their mobile banking services to increase their customer base in India. Also, Authors (Mpinganjira, M., & Bwalya, K. J. 2019), identify the factors influencing the adoption of mobile banking in South Africa. The authors conducted a survey of 400 bank customers in South Africa to collect data on their adoption of mobile banking and their attitudes towards it. The study identified several factors that influence the adoption of mobile banking, between them are perceived utility, expected usability, trust, social impact, and demographic elements.

The study indicated that the most important elements influencing the adoption of mobile banking were perceived utility and perceived simplicity of use. Other important factors included trust in the bank, social influence, and demographic factors such as age, income, and education level. The study also found that security concerns were a significant barrier to the adoption of mobile banking (Almadhun et al. 2019).

Overall, the study provides valuable insights into the factors influencing the adoption of mobile banking in South Africa. Banks and financial institutions can use this information to develop effective marketing strategies and improve their mobile banking services to increase their customer base in South Africa.

This study (Wan Yusoff, W. H., & Kassim, E. S. 2019), aims to examine the impact of perceived value and trust on mobile banking adoption in Malaysia. The authors conducted a survey of 300 bank customers in Malaysia to collect data on their adoption of mobile banking and their attitudes towards it. The study focused on the role of perceived value and trust in the adoption of mobile banking. The study found that perceived value and trust were significant predictors of mobile banking adoption in Malaysia. Perceived value was found to be positively related to mobile banking adoption, while trust was found to be negatively related to mobile banking adoption (Venkatesh et al. 2013 & Rmis et al. 2021& Almadhun et al. 2019).

- Research Methodology And Data Analysis

This section provides an overview of the nature of quantitative research, which involves the use of raw data to answer survey questions and minimize research results. The paragraph also highlights the importance of survey research in understanding clients’ skills or ideas over a period. The paragraph further notes that survey research can be used to investigate people’s behavior, attitudes, and thoughts, and that some studies aim to find a link between respondents’ characteristics and their behavior.

- Research design

This paragraph discusses the research design of the study, which is an explanatory study. The purpose of an explanatory study is to establish relationships between variables and to determine the cause and effect of one or more variables. The study focuses on specific phenomena over a period, making it a straightforward research design. The goal of the study is to determine how the term of mobile banking and its effects on customer satisfaction in Libya are influenced by perceived advantage, estimated simplicity for users, risk perception, consistency, and knowledge. The text also mentions that the study investigates the connection among independent as well as dependent factors.

- Target population

the target population for the study, which is the customers of four different Libyan banks, namely the Foreign Bank of Libya, National Commercial Bank, Libya National Bank, and Arab Group Bank. The study focuses on individual customers who have savings accounts with these banks, and the main characteristics of the target group are age, gender, educational level, and use of mobile banking. To define population as a group with certain characteristics, such as people, institutions, hospitals, shops, universities, etc. The notes that part of the survey analysis is related to individual customers, as the survey is based on the general behavior of each customer, which reflects their behavior more accurately.

- Sample Size

The sample size for the study. The focus of the study is on the commercial banking customers of the four selected Libyan banks, which were chosen based on their innovative approach to mobile banking services and their active and important behavior towards mobile banking. The author notes that the selected banks’ service time on these new platforms is longer than on other banks, and the proposed design can explain the consequences of this behavior. The study aims to encourage and understand citizens by highlighting the benefits of mobile banking and to provide non-mobile banking users with the best representation and knowledge to experience the mobile banking experience.

- Sampling Techniques

The total number of valid questionnaires used in the analysis was 400. Additionally, 20 questionnaires were not used in the analysis because respondents indicated that they did not use mobile banking, and therefore, these questionnaires were rejected and not included in the research analysis. This information suggests that the final sample size for the study was 400 respondents who were customers of the four selected Libyan banks and used mobile banking services.

- Data Collection and Analysis

The questionnaire used in the study consists of 28 items, which are divided into two parts. The first part includes four general information questions, while the remaining 25 questions relate to personal skills and customer satisfaction when purchasing mobile banking services. The questionnaire was designed to be short and simple, answering a few frequently asked questions, including more complex questions. The Likert scale was used as a response format, where respondents could indicate their behavior by checking whether they fully agree with the written information. The survey used a scale with values ranging from 1 (which indicated significant disagreement) to 5 (which indicated strong agreement). The questionnaire has been adjusted from appropriate studies with the goal of ensuring agreement with previous tests. The measurement of the respondents’ perception of these structural details is briefly discussed in the literature and in model models.

The study employed the SPSS software package to analyze the value data. Multiple linear regression analysis was conducted to examine the relationship between dependent and independent variables, also test research by hypotheses. The results of the statistical analysis were presented using tables, percentages, frequency distributions, and graphs to analyze the personal characteristics of the respondents. The SPSS 25.0 software version was utilized to obtain the results . ( Almadhun et al. 2021).

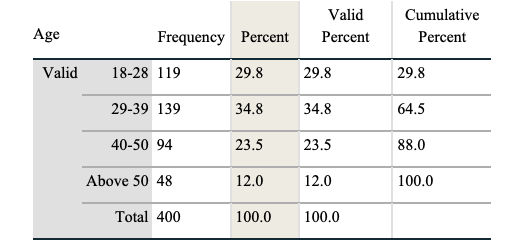

The information is presented in Table 1, the distribution of the study participants according to their age.

Table 1: Age distribution

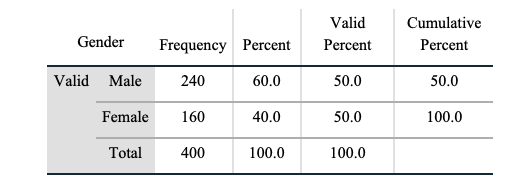

This table 2, describes the distribution of the study participants according to gender. The information shows that 60% male besides 40% female.

Table 2: gender distribution

Table 2: gender distribution

Results and Discussion

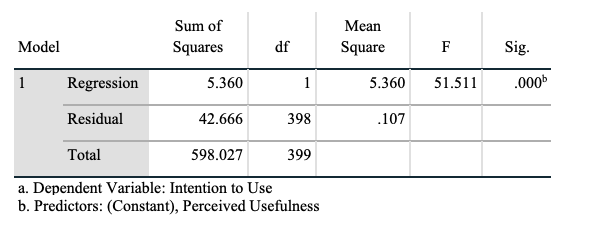

- H1: The perceived usefulness of mobile banking has a significant positive impact on users’ intention to use it.

Table 3: ANOVA (H1)

The results of the ANOVA test conducted for the regression model used to explain the variability of the dependent variable, intention to use mobile banking services. According to the table provided, the ANOVA test results showed that the regression model successfully explained the variation in the dependant variable. A substantial F-value of 51.511 and a p-value of 0.000, both below the given level of significance of 0.05, served as proof of this. This suggests that the model is statistically significant and can be used to predict the intention to use mobile banking services based on the independent variables included in the model. The results of this test provide support for the use of the regression model in examining the relationship between perceived usefulness and the intention to use mobile banking services, as stated in the hypothesis.

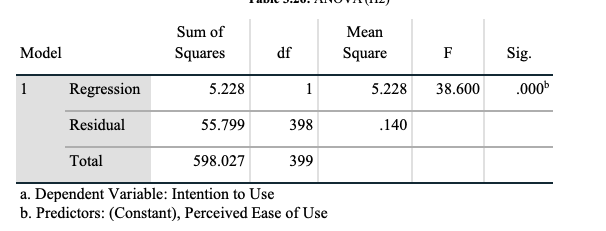

- H2: The perceived ease of use of mobile banking has a significant positive impact on users’ intention to use it.

Table 4: ANOVA (H2)

The table below displays the ANOVA test results, which demonstrate that the regression model was successful in accounting for the variation in the dependent variable. A p-value of 0.000 and a statistically significant F-value of 38.600 were used to demonstrate this, which is lower than the intended significance threshold of 0.05. This suggests that the model is statistically significant and can be used to predict the intention to use mobile banking services based on the independent variables included in the model.

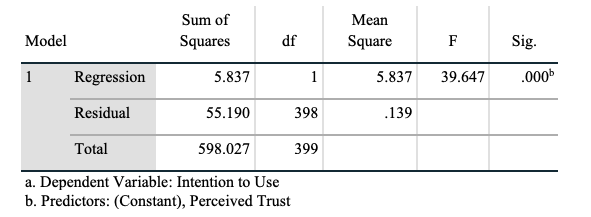

- H3: The perceived trust in mobile banking has a significant positive impact on users’ intention to use it.

Table 5: ANOVA (H3)

The regression model successfully accounted for the differences in the dependent variable, as evidenced by the outcome of the ANOVA test that appear in the above table. High proof that the model is statistically significant may be seen in the F-value of 39.647 and the extremely significant p-value of 0.000, which is below the significance level of 0.05. As a result, the independent variables of the model may be utilized to accurately predict the desire of employing mobile banking services.

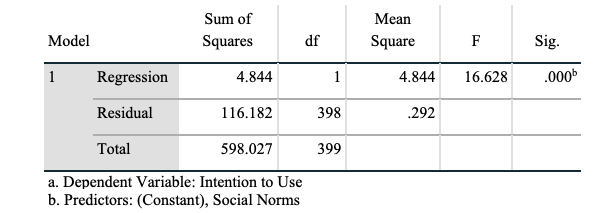

- H4: Social norms have a significant positive impact on users’ intention to use mobile banking.

Table 6 ANOVA (H4)

The statistics from the table’s analysis of variance indicate that the regression model did a good job of capturing the variation in the dependant variable. The model has an F-value of 16.628 and a significant p-value of 0.000, which is less than the significance level of 0.05. This indicates that the model is mathematically sound and can be trusted to predict the dependent variable based on the independent variables contained in the model.

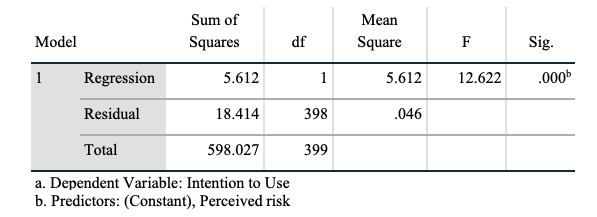

- H5: The perceived risk associated with using mobile banking has a significant negative impact on users’ intention to use it.

Table 7: ANOVA (H5)

The ANOVA test results indicate that a regression model can help explain the variability in the dependent variable, intention to use, based on the independent variable(s) in the model. Some key points:

1. F (1, 398) is the F-statistic, which tests whether the regression model is significant. The value of 12.622 means the model is significant.

2. The Sig. (0.000) value is the p-value, which tests the significance of the F-statistic. Since 0.000 is less than 0.05, we can conclude that at least one of the independent variables significantly predicts the dependent variable.

3. Since Sig. (0.000) < 0.05, we can say the regression model is statistically significant in explaining the variability in intention to use.

4. The F-statistic and p-value indicate that at least one of the independent variables in the regression model has a significant relationship with the dependent variable and helps explain its variability.

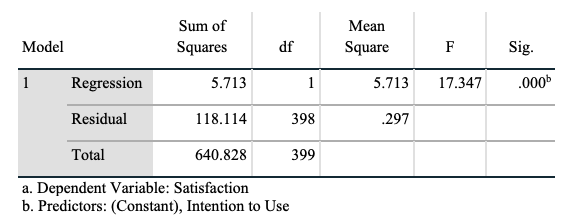

- H6: The degree to which consumers are satisfied with the service is significantly influenced by their propensity to use mobile banking.

Table 8: ANOVA (H6)

In accordance to the ANOVA table, the coefficient of variation for the given scenario is 17.347, which is a fairly large result. The numerator has 1 degree of freedom, whereas the factorization factor has 398 degrees of freedom. The p-value, shown as “Sig.” in the table, is 0.000, which suggests that it is less relevant than the threshold of 0.05. As a result, there is strong proof the model is statistically significant and that it may account for a sizable chunk of the variation in the dependent variable. “with intent to use.”

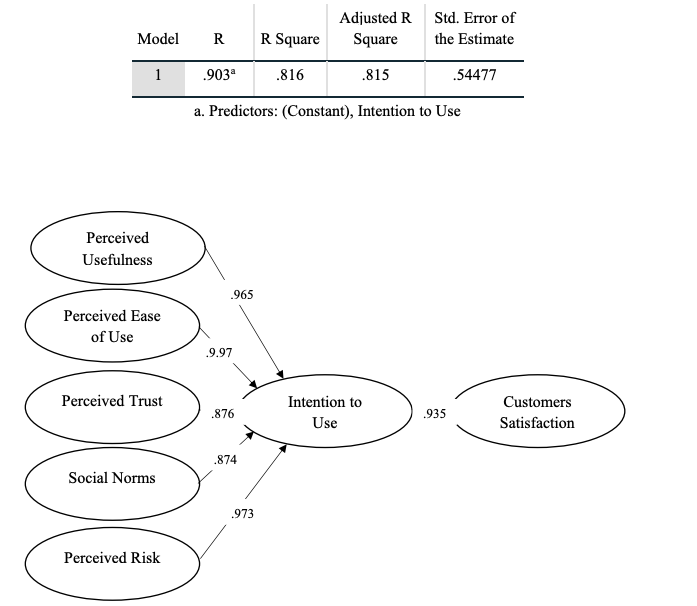

Based on the results presented in the model summary, it can be observed that the R-squared (R2) value is 0.816, indicating that the intention to use mobile banking services can explain 81.6% of the variation in customer satisfaction. The data also shows a mean correlation value of 0.903 across “intention to use” mobile banking features and satisfaction with the services, indicating a strong positive link between these two factors. These findings provide valuable insights into the relationship between the intention to use mobile banking services and customer satisfaction, which can aid banks and financial institutions in designing effective strategies to enhance customer satisfaction through the adoption of mobile banking services.

Figure 1: hypothesis testing results:

- Conclusion:

Based on the data analysis and the obtained results, several key findings can be drawn from this study. Firstly, while there is a general agreement that mobile banking provides benefits in terms of facilitating banking operations and transactions, these benefits are not perceived as being sufficient by users. Secondly, individuals find it easy to use mobile banking applications due to their design, but face difficulties in obtaining suitable mobile phones for the service application.

Thirdly, while there is a general confidence in using mobile banking applications, there is a lack of desire to conduct banking transactions through this application due to concerns over the safety of mobile phones for conducting these types of transactions. Fourthly, while there is a social impact of some kind on individuals to use the service, it is not necessarily related to their social status or standing.

Fifthly, the study found that there is a direct relationship between various factors such as perceived usefulness, perceived ease of use, perceived trust, social norms, perceived risk, and the intention to use mobile banking services. Finally, the study also found a direct relationship between the intention to use mobile banking services and customer satisfaction. Overall, these findings provide valuable insights for banks and financial institutions in understanding the factors that influence customer adoption of mobile banking services, and in designing strategies to enhance customer satisfaction through mobile banking services. Therefore, to encourage adoption of mobile banking services among the Libyan bank’s customers, the bank should focus on improving customers’ perceptions of these factors. For example, the bank could emphasize the benefits and convenience of mobile banking, ensure that the service is secure and reliable, and promote the service through positive social norms. Additionally, the bank could work to reduce customers’ perceived risks by addressing concerns related to security and privacy. By doing so, the bank may be able to increase adoption of its mobile banking services among its customers.

Reference

Adomako, S., Danso, A., & Damoah, I. S. (2018). Determinants of mobile banking adoption in Ghana. Journal of African Business, 19(4), 430-454. doi: 10.1080/15228916.2018.1474340.

Al-Sukkar, A., & Al-Wesha, S. (2019). Factors affecting the adoption of mobile banking in Jordan. Journal of Business Research, 98, 417-425. doi: 10.1016/j.jbusres.2019.01.022.

Almadhun, Salem Husein, Salem M Aldeep, Aimen M Rmis, and Khairia A Amer. “Examination of 4G (LTE) Wireless Network.” El tarbawe journal 19, no. 1 (July 2021): 285–94. https://doi.org/http://dspace.elmergib.edu.ly/xmlui/handle/123456789/1119.

Almadhun, Salem, Mehmet TOYCAN, and Ahmet ADALIER. “VB2ALGO: An Educational Reverse Engineering Tool to Enhance High School Students’ Learning Capacities in Programming.” Revista de Cercetare si Interventie Sociala 67 (2019): 67–87. https://doi.org/10.33788/rcis.67.5.

Hanan A. Khalil, Aimen M. Rmis, Salem H. Almadhun , Tareg A. Elawaj, Walid F. Naamat. (2023). The creation of theoretical frameworks to establish sustainable adoption of e-health in Libya. Humanitarian and Natural Sciences Journal, 4(7). doi:10.53796/hnsj4716

Kshetri, N. (2018). Blockchain’s roles in meeting key supply chain management objectives. International Journal of Information Management, 39, 80-89. doi: 10.1016/j.ijinfomgt.2017.12.008.).

Mpinganjira, M., & Bwalya, K. J. (2019). Factors influencing the adoption of mobile banking in South Africa. The Electronic Journal of Information Systems in Developing Countries, 86(2), e12072. doi: 10.1002/isd2.12072.

Research and Markets. (2021). Global Mobile Banking Market – Growth, Trends, COVID-19 Impact, and Forecasts (2021 – 2026).

Rmis, A. Alkazagli, M. Alloush. O. Almadhun, Salem. (2021). Sentiment Classification Using Three Machine Learning Models. Vol. 34 No. 1, June.

Rmis, Aimen & Topcu, Ahmet. (2020). Evaluating Riak Key Value Cluster for Big Data. Tehnicki vjesnik – Technical Gazette. 27. 10.17559/TV-20180916120558.

Shang, S. S., & Deng, Z. (2014). Understanding the adoption of mobile banking: An empirical study in China. Journal of Electronic Commerce Research, 15(1), 53-72.

Singh, P., & Srivastava, R. K. (2018). Factors influencing the adoption of mobile banking in India: an empirical study. Journal of Financial Services Marketing, 23(4), 187-196. doi: 10.1057/s41264-018-0044-1.

Topcu, Ahmet & Rmis, Aimen. (2020). Analysis and Evaluation of the Riak Cluster Environment in Distributed Databases. Computer Standards & Interfaces. 72. 103452. 10.1016/j.csi.2020.103452.

Venkatesh, V., Brown, S. A., & Bala, H. (2013). Bridging the qualitative-quantitative divide: guidelines for conducting mixed methods research in information systems. MIS Quarterly, X(X), 1-34.

Alloush, O. A. A., & Mahendrawathi, E. R. (2020). ERP Systems in Higher Education: A Systematic Literature Review. SISFO VOL 9 NO 2, 9.

https://doi.org/10.24089/j.sisfo.2020.01.003

Wan Yusoff, W. H., & Kassim, E. S. (2019). The impact of perceived value and trust on mobile banking adoption in Malaysia. Journal of Islamic Marketing, 10(1), 120-137. doi: 10.1108/JIMA-08-2017-0114.